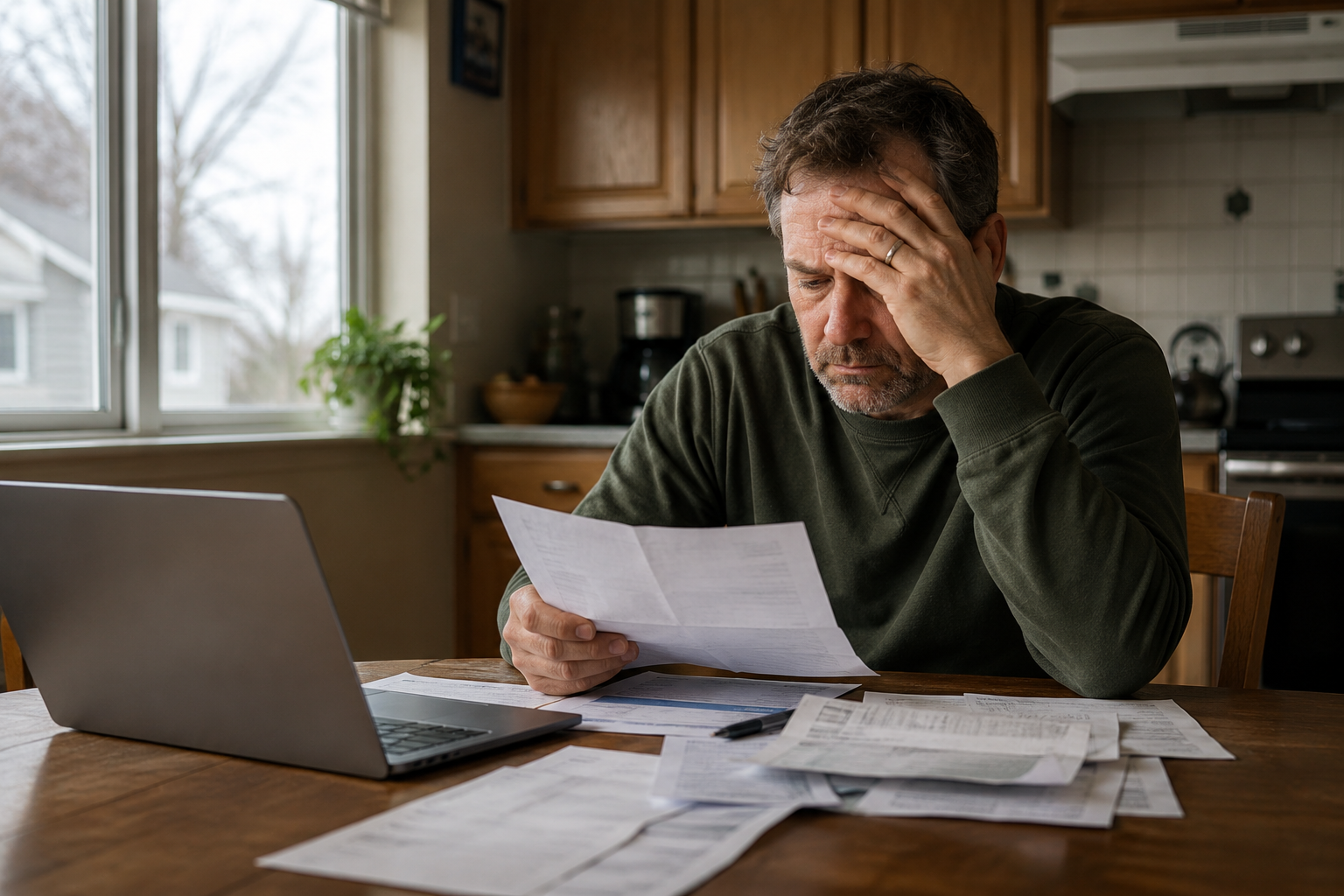

If you own a home in the Minneapolis-St. Paul area and have been trying to sell, you may have noticed something unsettling over the past year or two. The buyers who were eagerly snapping up homes are harder to find. Offers are slower to arrive. And the financial pressure you are feeling is not letting up while your home sits on the market.

The reason is no mystery. The average 30 year fixed mortgage rate is currently hovering around 6.61%. That means a buyer purchasing a $347,000 home with 20% down is looking at roughly $1,774 per month just in principal and interest, not to mention taxes and insurance. For many would-be buyers, that number simply does not work. So they wait. And while they wait, you are stuck.

THE RATE TRAP EXPLAINED

When rates were near 3%, a buyer could afford significantly more home for the same monthly payment. Today, that same payment buys far less. The pool of qualified buyers has shrunk, and the buyers who are still active have options. The Twin Cities market has seen an 18% surge in active listings in 2026, and homes are now sitting on the market an average of 45 to 52 days. That is a significant shift from the frenzy of recent years.

What this creates for sellers in financial distress is a compounding problem. You need to sell. The market has slowed down. And every month that passes adds more costs, more stress, and potentially more damage to your financial situation.

WHO FEELS THIS THE MOST

Not every homeowner is equally affected by this dynamic. If you have significant equity and no urgency, you can afford to wait it out. But many Twin Cities homeowners do not have that luxury. This trap hits hardest when you are dealing with any of the following situations.

You are behind on mortgage payments and watching a foreclosure timeline close in. You are going through a divorce and the home needs to be sold as part of a settlement. You have inherited a property and cannot afford to carry the taxes, insurance, and maintenance. You are a landlord who is tired of the headaches and wants out. You have a major repair looming that you cannot afford to fix before listing.

In all of these cases, listing your home on the traditional market and waiting 45 to 52 days for a qualified buyer to show up, then waiting another 30 to 45 days to close, is a timeline that can cause serious financial harm.

WHAT THE TRADITIONAL MARKET LOOKS LIKE RIGHT NOW

Even when buyers do show up, they are in a stronger negotiating position than they have been in years. Sellers are increasingly offering concessions, price reductions, and other incentives just to get deals across the finish line. If your home needs work, or if you are dealing with a complicated situation like probate or divorce, your negotiating position is even weaker.

Buyers who are financing a purchase through a traditional mortgage are also subject to appraisals, inspections, and lender requirements. If your home has deferred maintenance, structural issues, or code problems, those hurdles can kill a deal entirely or force you to spend money you do not have just to get to the closing table.

HOW A CASH SALE BREAKS THE TRAP

Selling your home for cash to a direct buyer like Homefield Homebuyers sidesteps the rate problem entirely. We do not use mortgage financing. That means there is no waiting for a bank to approve a buyer, no appraisal contingency, and no risk of a deal falling apart because rates moved or a buyer got cold feet.

We buy homes as-is, which means you do not need to make repairs or updates before selling. We can close on your timeline, which is especially important if you are facing a foreclosure sale date, a court order related to divorce, or a probate deadline. And because we make a straightforward cash offer, you know exactly what you are getting without the uncertainty of a traditional listing.

THE NUMBERS THAT MATTER TO YOU

The question most homeowners ask is whether a cash offer will be lower than what they could get on the open market. It is a fair question. The honest answer is that a cash offer may be lower than a top-dollar listing price in a hot market. But a cash offer needs to be compared against what you would actually net after agent commissions, closing costs, repair requests, price reductions, carrying costs during a 45-to-52-day listing period, and the emotional and financial toll of uncertainty.

When you run those numbers, the gap often closes significantly. And when you factor in the risk of a deal falling through or a foreclosure moving forward while you wait, a fast and certain cash sale frequently comes out ahead.

WHAT TO DO IF YOU ARE FEELING STUCK

If rising rates and a slower market have left you feeling trapped, the first step is simply to understand your options. You do not have to commit to anything just to find out what your home is worth to a cash buyer. Homefield Homebuyers serves homeowners throughout the Twin Cities metro and can walk you through the process with no pressure and no obligation.

If your situation involves foreclosure, divorce, an inherited property, or another time-sensitive issue, do not wait for the market to turn in your favor. The carrying costs and risks of waiting almost always outweigh the potential upside. Reach out to us through our contact us page to start a conversation about your options.

Visit HomefieldHomebuyers.com and fill out our contact form or send us an email at Sales@homefieldhomebuyers.com to get started.

Comments